A new report suggests Canadian telecom prices have dropped dramatically since 2020, claiming a 65 percent reduction. Commissioned by a group representing major Canadian carriers and infrastructure companies, the study by Price Waterhouse Coopers (PWC) analyzed the Canadian market. However, this claim faces scrutiny, as many Canadians may not have seen a significant decrease in their monthly bills.

Contents

This analysis delves into the PWC report’s findings, contrasts them with consumer experience and other data, and explores the implications for the Canadian wireless market and future regulation.

Deconstructing the Claim: Are Prices Really Down 65%?

The PWC report asserts that the average monthly price for 10GB of data in Canada is now $28. This figure is based on what appears to be an average cost-per-gigabyte calculation across various plans, rather than the typical cost most Canadians pay for their actual service.

Critically, the study was commissioned by the Canadian Telecommunications Association (CTA), an industry group. While PWC conducted the study independently, some observers note the report omits key market factors that could present a less favorable picture of carrier pricing, such as rising roaming charges or the CRTC’s recent efforts to boost competition. This isn’t the first time telecom CEOs have made similar claims about price drops to regulators, leading the CRTC to update how it tracks wireless pricing.

Looking at the market, the cheapest 10GB plans are often found on flanker brands like Public Mobile (Telus-owned) or Lucky Mobile (Bell-owned). While Public Mobile offers a 10GB plan around $30, and Lucky Mobile has a 15GB plan for $29, these brands are less known and used than their parent companies. App download numbers, though not a perfect metric, suggest main carrier apps (Bell: 10M+ downloads) are significantly more popular than flanker brand apps (Lucky Mobile: 500,000+ downloads).

The Marketing Gap: Why Cheaper Plans Aren’t Reaching Everyone

The report highlights a disconnect between the theoretical ‘price per gigabyte’ drop and the actual cost for consumers. While the price per GB on large data plans ($60 for 120GB+) has indeed fallen, the major carriers (Bell, Rogers, Telus) primarily market these higher-data, higher-cost plans on their main websites and through extensive advertising.

Canadians who aren’t deep into comparing mobile plans or aware of the relationship between major carriers and their flanker brands often default to the big three. This means they miss out on potentially more affordable options offered by brands like Fido (Rogers-owned), Koodo (Telus-owned), Virgin Plus (Bell-owned), or Freedom Mobile, which often provide plans with data allowances better suited to average usage at lower price points. The lack of prominent promotion for flanker brands on the main carrier sites contributes to this confusion.

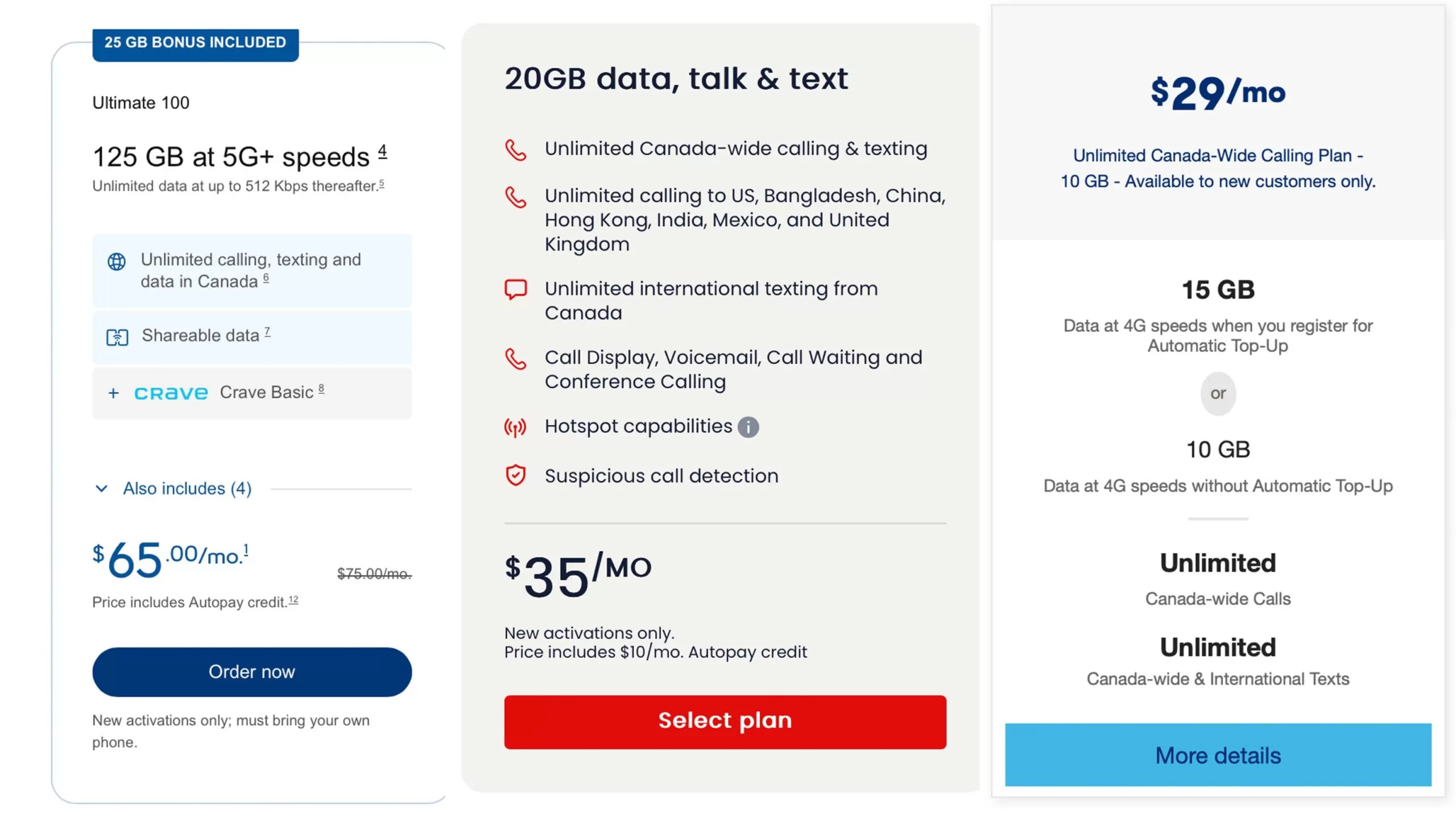

Comparison of various wireless plans offered by different brands under the same parent company

Comparison of various wireless plans offered by different brands under the same parent company

For example, a consumer using only a few gigabytes per month might find that the cheapest plans available from the main carriers are far more data than they need, resulting in a monthly bill higher than necessary, even if the cost per gigabyte on that plan is low.

What Canadians Actually Pay: The ARPU Perspective

Instead of focusing solely on the price per gigabyte, a more telling metric for what consumers actually pay is Average Revenue Per User (ARPU). This figure reflects the average amount a telecom company earns from each subscriber per month.

According to CRTC reports, the average revenue per mobile phone user in Canada was $66.70 in 2020. By 2023, this number had increased to $70.23. While major carriers report their wireless ARPU around $58-$60 in their most recent financials (potentially excluding device financing costs included by the CRTC), the CRTC’s data over the past few years shows an increase in what subscribers pay on average, not a 65 percent decrease.

Graph showing the average monthly data usage per Canadian wireless subscriber over time

Graph showing the average monthly data usage per Canadian wireless subscriber over time

Considering the PWC report notes that the average Canadian uses only 9GB of data per month, the prevalence of expensive plans offering 100GB+ highlights a mismatch between market offerings and typical needs. If the cost per gigabyte is truly low, one might expect to see more widely available 10-15GB plans priced under $30.

Broader Implications: Regulation and Competition

Stepping back, the PWC report seems to frame the telecom sector’s challenges – economic conditions, trade issues, climate change – as reasons to advocate for fewer regulations and increased investment, drawing comparisons between the highly regulated EU market and the less regulated U.S. market. However, the report selectively omits mentioning positive outcomes of EU regulation, such as lower prices and significant consumer benefits like standardized charging ports.

Other crucial developments in the Canadian market are also not discussed. The debate around increasing roaming charges, which even led to carriers presenting their case to the CRTC, is notably absent. Furthermore, the CRTC’s recent push to increase competition by requiring major carriers to provide wholesale access to their fiber network infrastructure for competitors (allowing companies like Telus to use Bell lines) is not covered. This regulatory change has already increased internet choices for thousands of Canadians, prompting reactions from carriers, such as Bell’s announced reduction in future infrastructure investments in response to the wholesale access requirement.

This context, alongside the major telecoms reporting an average of $6 billion each in free cash flow in 2024, paints a more complex picture than the simple narrative of plummeting prices and industry challenges suggests.

What’s Next?

While the price per gigabyte for large data buckets has decreased in Canada, the actual average cost for a Canadian telecom subscriber, as indicated by ARPU data, has remained relatively stable or even slightly increased over the last few years. The challenge lies in the market structure and marketing strategies that steer consumers towards higher-cost plans, even when cheaper alternatives (often from the same parent company’s flanker brands) exist.

Future developments will likely center on whether the CRTC’s efforts to increase competition, particularly through wholesale network access, will genuinely lead to lower prices for consumers across all plan types, or if the market structure will continue to favor the higher-revenue main brands and their large data plans. Consumers should continue to compare plans across main brands and flankers, keeping average monthly cost and actual data usage in mind, rather than solely focusing on the cost per gigabyte.

For related analysis on Canadian telecom policies and market trends, explore:

- Previous discussions on telecom price claims

- How the CRTC changed its wireless pricing tracking

- Reports on CRTC efforts to increase competition