A new study from the University of Waterloo presents a compelling argument: skyrocketing rent increases in Toronto are being driven less by traditional market forces and more by the aggressive strategies of large financial landlords. This research dives deep into how real estate investment trusts (REITs), private equity firms, and asset managers are leveraging their scale and tactics to maximize rent extraction, acting more like an oligopoly than participants in a competitive market. The key takeaway? This financialization of housing is worsening shelter instability, particularly for vulnerable populations.

Contents

Decoding Toronto’s Rental Market Dynamics

Researchers from the School of Planning at the University of Waterloo analyzed data from 1,600 apartment buildings across Toronto between 2022 and 2024. They broke down rental trends by neighbourhood and, crucially, by the type of landlord – comparing large financial firms to traditional operators like family-run businesses and individual “mom & pop” landlords.

Going beyond simple market data, the study incorporated insights from interviews, corporate filings, and real estate industry transcripts. This approach aimed to understand the strategies and motivations of key players, revealing a rental market dynamic far more complex than basic supply and demand economics.

The Financial Landlord Premium: Higher Rents and Faster Growth

The study found a significant “premium” charged by financial landlords. On average, these firms demanded 44% more than the neighbourhood’s average rent, translating to roughly $670 extra per month. This far outstrips the premiums charged by family chains (30%) or individual landlords (15-22%). The researchers suggest that because these large firms often cluster and base pricing on comparable properties, their high rates accelerate rent inflation across entire areas.

Chart showing significant rent premiums charged by financial landlords compared to other types in Toronto.

Chart showing significant rent premiums charged by financial landlords compared to other types in Toronto.

Looking at quarterly rent increases, the disparities are stark:

- Financial landlords: Average 5.04% increase per quarter, an annualized rate of 21.52%.

- Family-run chains: 4.99% per quarter.

- Single-property owners: 3.61% per quarter.

- Non-profits: 1.0% per quarter.

Using statistical models, the study concluded that the same rental unit would cost approximately 13.8% more if owned by a financial firm compared to an individual landlord. “If a unit held by a Single Owner… was listed at our dataset’s average rent—$2,187, the expected rent of the same unit would be $2,510 if it were owned by a financial firm, a $323 difference,” explained authors Martine August and Cloé St-Hilaire.

Targeting Vulnerable Communities for Profit

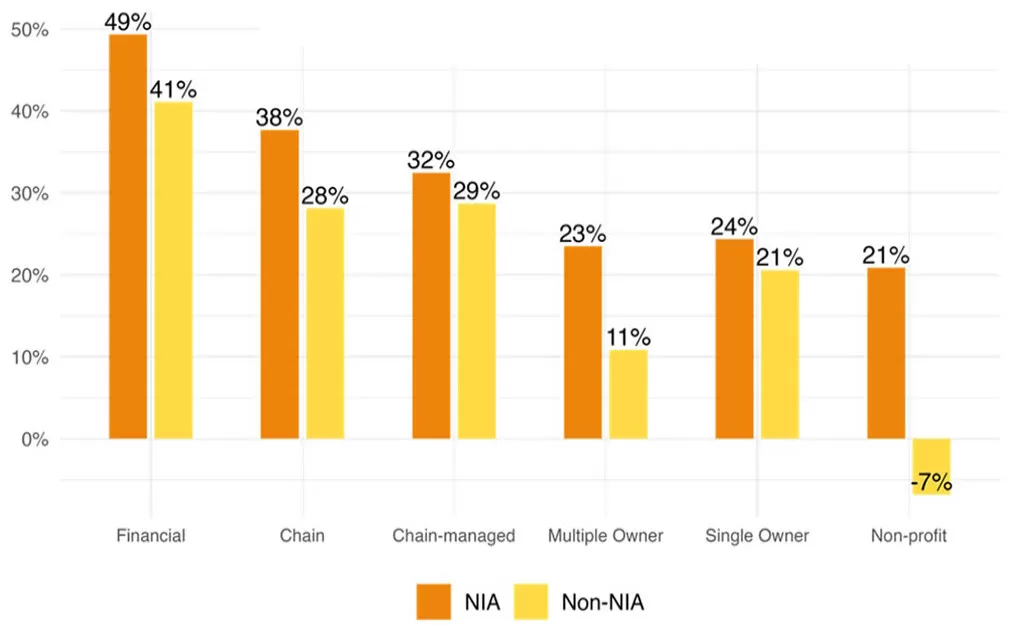

The research highlights a concerning pattern: financial landlords appear to be specifically targeting Toronto’s designated Neighbourhood Improvement Areas (NIAs). These are typically low-income, racialized districts that have historically offered more affordable housing options.

In these NIAs, financial firms charged rents 20% higher than other landlords, effectively capturing the “rent gap” – the difference between current affordable rents and the higher market rates they believe can be achieved. This strategic focus allows financial landlords to exert a disproportionate influence on these neighbourhoods. As the authors starkly put it, “While tenants face a crisis, the shareholders and senior executives in financial firms investing in rental housing gather diamonds.”

Tactics of Extraction: Algorithms and Displacement

Financial landlords employ a mix of modern technology and aggressive strategies to boost returns. A notable tool is algorithmic pricing software like YieldStar, which adjusts rents based on local conditions and projected demand. Researchers found evidence suggesting this software can even recommend keeping units vacant temporarily to artificially constrain supply and push prices up.

This algorithmic approach has attracted scrutiny, with the US Department of Justice pursuing an antitrust case against YieldStar’s parent company, alleging the software facilitates collusion among large landlords to coordinate price increases. (The company denies these allegations).

Beyond algorithms, some financial landlords openly discuss “value add” and “repositioning” strategies. This often involves renovating units to justify substantial rent hikes, sometimes leading to the displacement of existing tenants. While superficially more polished, this mirrors the tactics seen in “renovictions,” albeit on a larger, more systematic scale by well-funded entities.

Financialization’s Grip and Policy Paradox

The study concludes that financial landlords are directly contributing to higher rents and eroding affordability in Toronto. The trend of housing financialization, which gained momentum with low interest rates, has led to financial firms acquiring a dominant share of the rental market in recent years. This increasing market concentration amplifies their ability to dictate prices.

Ironically, instead of implementing policies to regulate the growth and practices of these large firms, the study suggests that policymakers are sometimes using public resources to support their expansion. This approach, framing the financialization of rentals as a “solution” to affordability issues, raises questions about whether shelter instability is becoming an unintended, or even accepted, outcome of current policy.

The research provides a critical lens on the forces shaping Canada’s — and increasingly, global — rental markets, urging a deeper look at the role of financialization beyond simple supply and demand narratives.

To learn more about housing market trends and policy impacts, explore related articles on this topic.