Florida’s condominium market, a significant part of the state’s housing sector, is currently experiencing a notable downturn. After a period of strong growth following the pandemic, condo sales and prices have fallen considerably from their peaks. This weakness is more pronounced than in the single-family home market and is linked to several factors, including new building regulations, rising costs, and shifting migration patterns.

Contents

Key Takeaways:

- Florida condo sales are down significantly, and prices are trailing lower compared to recent peaks and other housing segments.

- Inventory levels for condos are surging, indicating a strong buyer’s market.

- Higher interest rates, slowing domestic migration, and soaring home insurance premiums are affecting the broader Florida market, but condos face added burdens from rising HOA fees and costs tied to new inspection and repair laws.

- While conditions are expected to remain weak near-term, potential relief from lower interest rates, a rebound in migration, and recent adjustments to the inspection law could pave the way for a gradual recovery by late 2026.

Condo Weakness Deepens as Sales Fall and Inventory Builds

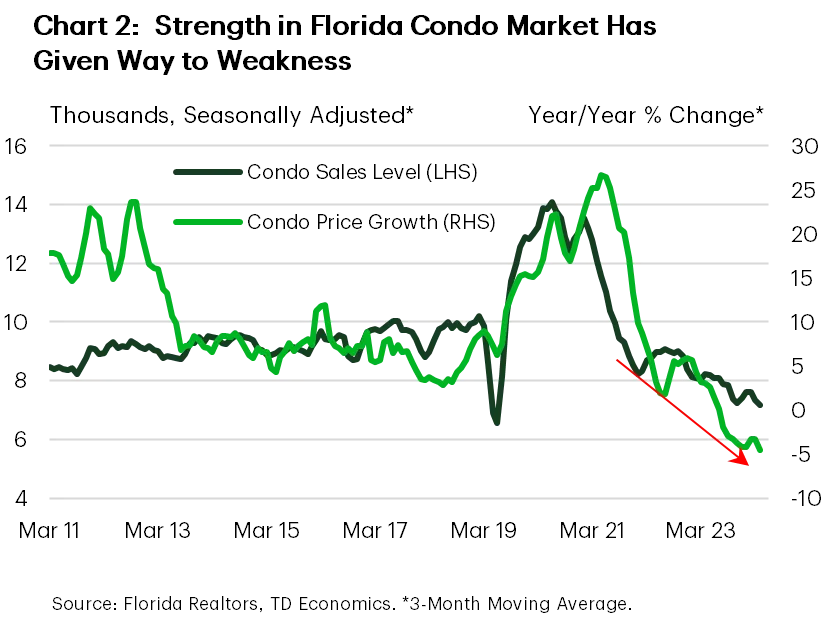

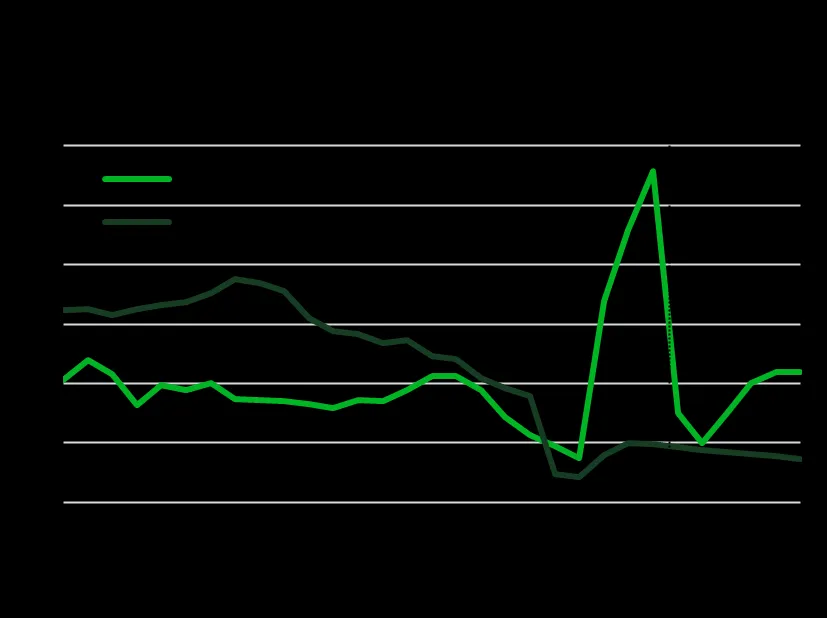

Florida’s condo and townhome market, once a dynamic segment, has seen a dramatic reversal. Compared to pre-pandemic levels (2018-19), state condo sales are down by over a quarter, and year-over-year figures show a 13% decline in the last three months. Median condo prices have also dropped, falling about 8% from their peak and down 4.5% year-over-year. This contrasts sharply with Florida single-family homes (-2% y/y) and the overall U.S. condo market (+2% y/y), highlighting the specific challenges facing Florida condos.

Chart showing Florida single-family and condo market performance, highlighting significant declines in Florida condo sales and prices.

Chart showing Florida single-family and condo market performance, highlighting significant declines in Florida condo sales and prices.

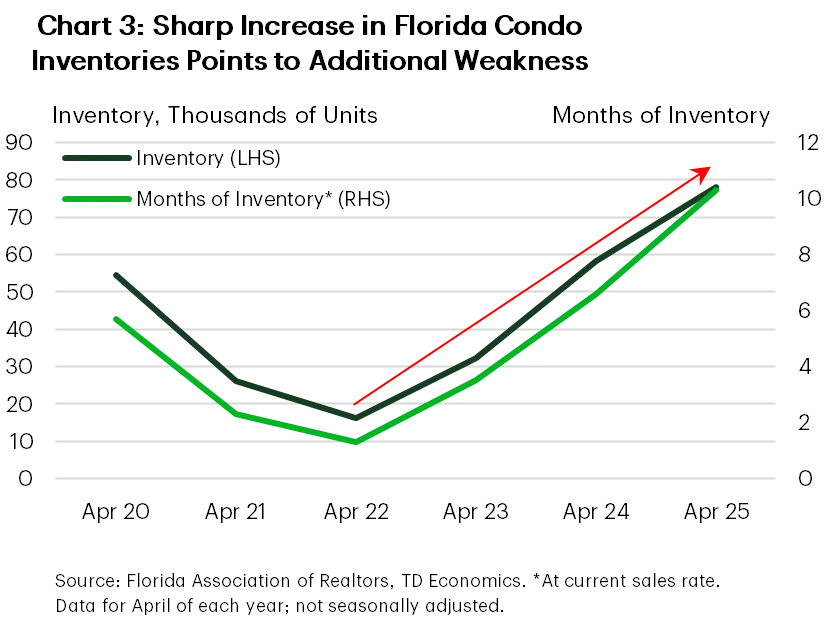

A major indicator of the market shift is the surge in inventory. Nearly 80,000 condos and townhomes are currently for sale across Florida, a 35% increase from a year ago. This amounts to over 10 months of supply based on current sales rates, a significant jump from recent years and well above the 5.6 months of supply for single-family homes. This excess inventory firmly places the condo market in buyer’s territory.

Graph illustrating the decline in Florida condo sales volume and year-over-year median price change since the post-pandemic peak.

Graph illustrating the decline in Florida condo sales volume and year-over-year median price change since the post-pandemic peak.

Multiple Headwinds Impacting the Market

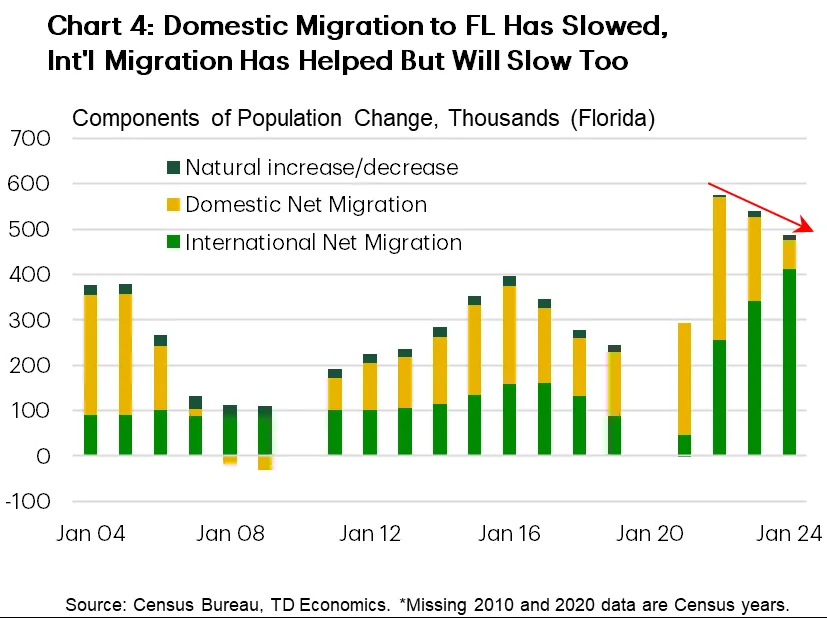

Several factors are weighing on the broader Florida housing market, including elevated mortgage rates near 7% and increased economic uncertainty, contributing to buyer hesitation. Domestic migration into the state also slowed significantly last year, reaching its lowest level since the Great Financial Crisis, although increased international migration helped offset some of this. Furthermore, Florida continues to have the highest home insurance premiums in the U.S., with condo-specific premiums at least double the national average, adding considerable cost for owners.

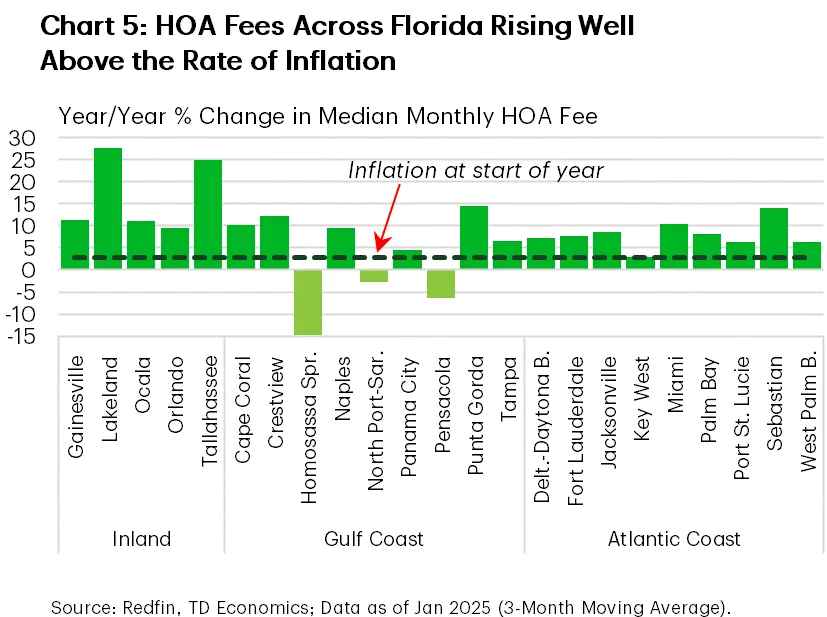

The condo sector faces additional, unique pressures. Homeowner Association (HOA) fees have been rising rapidly, partly due to general inflation, but also significantly impacted by new regulations. Recent legislative changes require older condo buildings (30+ years old, 3+ stories) to undergo mandatory structural integrity inspections, and associations must fund necessary repairs. These inspections often uncover underlying issues, leading to sharp increases in regular HOA fees or substantial ‘special assessments’ charged to unit owners. This financial burden is a major deterrent for potential buyers and a push factor for existing owners to sell, further swelling the inventory.

Bar chart displaying the significant increase in Florida condo inventory levels and months of supply in recent years.

Bar chart displaying the significant increase in Florida condo inventory levels and months of supply in recent years.

Inadequate insurance coverage or insufficient reserve funds uncovered during inspections can also lead to condo associations being placed on confidential “blacklists” by mortgage entities like Fannie Mae. This severely restricts access to mortgage financing for units in these buildings, drastically limiting the pool of potential buyers and perpetuating the market downturn.

Chart detailing Florida's population change drivers, showing a recent slowdown in domestic migration inflows.

Chart detailing Florida's population change drivers, showing a recent slowdown in domestic migration inflows.

Reports also suggest that foreign owners, particularly Canadian “snowbirds,” are looking to sell their Florida properties. While many foreign buyers use cash and are less affected by interest rates, they are still subject to rising HOA fees and repair costs. A weaker Canadian dollar and other factors may also contribute to this trend, potentially adding to the state’s growing condo inventory.

Graph comparing year-over-year HOA fee growth across major Florida metro areas, indicating increases exceeding inflation.

Graph comparing year-over-year HOA fee growth across major Florida metro areas, indicating increases exceeding inflation.

Condos’ Significant Role in Florida’s Housing Landscape

Condos and townhomes constitute a much larger portion of Florida’s housing market compared to the national average. The state is home to about 1.5 million condo units, making up one-fifth of the nation’s total condo stock and roughly 15% of Florida’s total housing stock – more than double the national share. In recent years, condos have accounted for over a quarter of all home sales in Florida, significantly higher than the roughly 10% share country-wide.

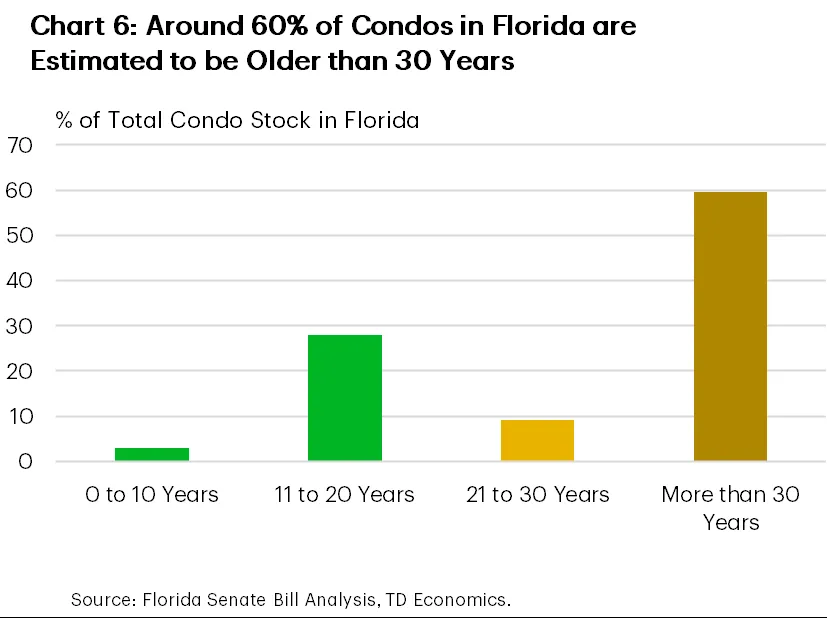

Chart illustrating the age breakdown of Florida's condo inventory, indicating a large percentage of older buildings.

Chart illustrating the age breakdown of Florida's condo inventory, indicating a large percentage of older buildings.

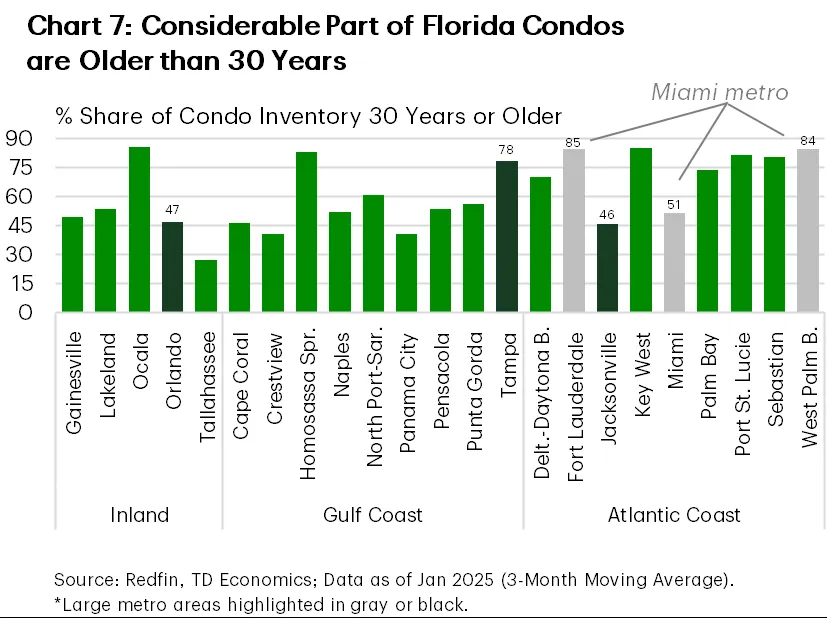

A key factor linked to the new regulations is the age of the condo stock. Over half of Florida’s condo units, around 900,000 units managed by some 16,000 associations, are older than 30 years. This means a large portion of the state’s condo inventory is potentially affected by the stricter inspection and repair requirements. While the exact share varies by location, major metro areas like Fort Lauderdale and West Palm Beach have a particularly high concentration of older condos, with estimates reaching 85%.

Bar chart showing the high percentage of condos over 30 years old in selected Florida urban areas.

Bar chart showing the high percentage of condos over 30 years old in selected Florida urban areas.

Economic Impact and Potential Mitigation

The financial burden of mandatory inspections and repairs will impact condo owners and the broader Florida economy to varying degrees. Owners may need to use savings or cut back on other spending to cover costs, which could weigh on consumer spending and moderate the state’s economic growth. The most vulnerable properties are those blacklisted by mortgage backers due to major repairs, inadequate reserves, or insufficient insurance, making it extremely difficult for owners to sell.

However, some mitigating factors exist. Certain areas, like Miami-Dade and Broward counties, already had similar inspection requirements, albeit less stringent. The urgency for repairs also creates opportunities for the construction and related industries. Additionally, as more units become difficult to sell, some inventory may shift to the rental market, potentially offering some relief for renters.

Glimmers of Hope for a Medium-Term Recovery

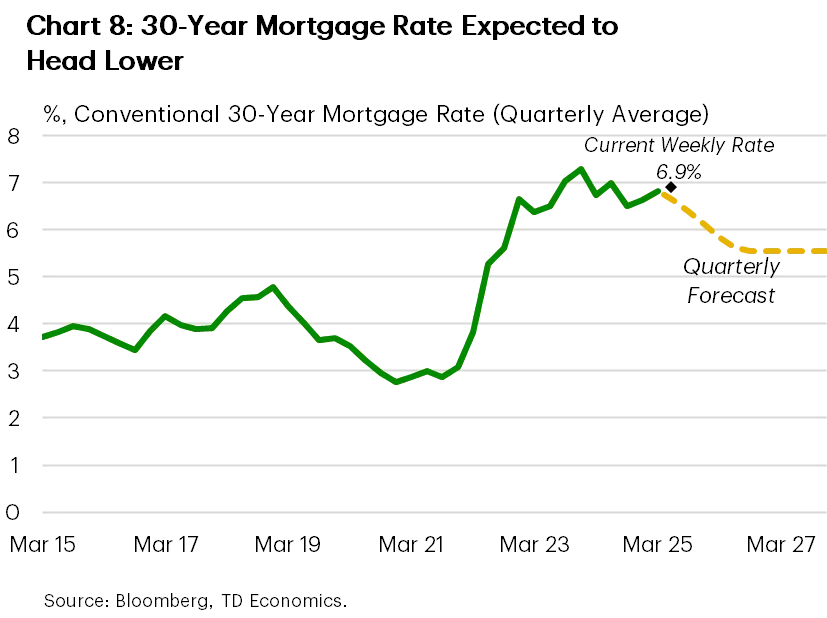

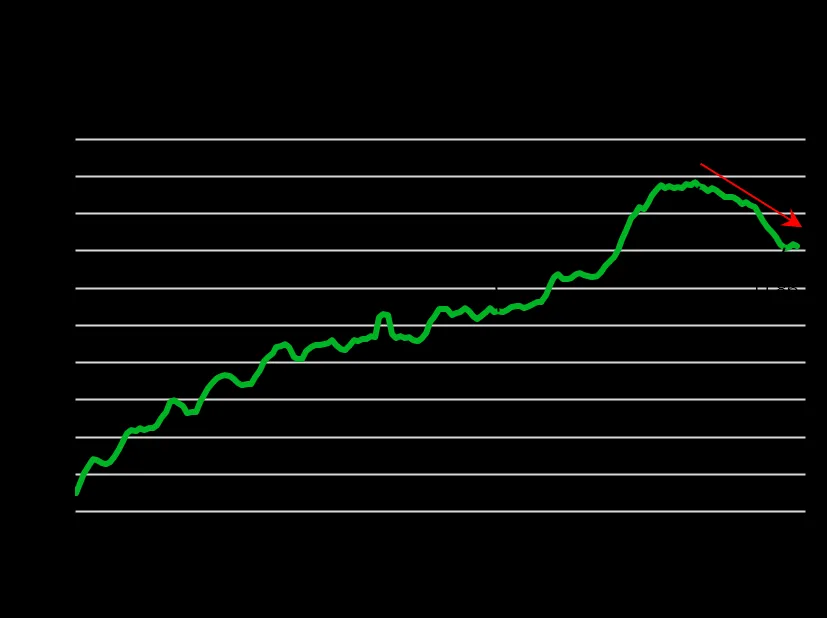

While the near-term outlook for the Florida condo market remains challenging, several factors could set the stage for a gradual recovery by late 2026. Expectations for lower interest rates in the coming quarters are a significant positive. Assuming the Federal Reserve begins trimming rates in the latter half of 2025, mortgage rates could fall into the 5.5-6.0% range by the end of next year, providing a boost to affordability across the housing market, including condos.

Graph showing historical and forecast trends for 30-year mortgage rates, projecting a future decline.

Graph showing historical and forecast trends for 30-year mortgage rates, projecting a future decline.

International migration inflows to the U.S., an important source of buyers and residents for Florida, are expected to firm up again in about two years, supporting housing demand. While domestic migration trends are less clear, Florida’s dynamic economy, which is projected to continue outperforming the nation with lower unemployment, should help attract residents over time. An underperformance in Florida condo prices relative to the national average could also make the state a more attractive destination down the road.

Chart forecasting US net migration trends, showing an expected easing followed by a rebound.

Chart forecasting US net migration trends, showing an expected easing followed by a rebound.

Finally, recent adjustments to the state law (HB 913) regarding structural inspections could ease some immediate pressure. The bill extends the deadline for studies, allows associations to use loans for reserve obligations, and permits a two-year pause in reserve funding after inspections. These changes aim to make repair costs more manageable for associations and owners in the near term, although the ultimate financial responsibility still falls on unit holders.

Graph comparing Florida median condo prices to the US median, showing Florida's recent price underperformance.

Graph comparing Florida median condo prices to the US median, showing Florida's recent price underperformance.

Bottom Line

The downturn in the Florida condo market is a complex issue driven by a confluence of factors. Stricter building regulations requiring potentially costly inspections and repairs have undoubtedly exacerbated the situation, particularly for the state’s abundant older condo stock. However, broader economic headwinds like elevated interest rates, slower domestic migration, and reduced interest from some international buyers also play significant roles.

In the short term, the market is likely to remain weak, characterized by falling sales and a rising glut of inventory. Yet, recent amendments to the inspection law offer some immediate relief. Looking ahead, the prospect of lower interest rates and an eventual rebound in migration patterns, coupled with Florida’s expected economic resilience, provides a basis for a gradual recovery in the condo market by late 2026.

- For more insights into the Florida housing market, explore related articles on [link to related article 1] and [link to related article 2].