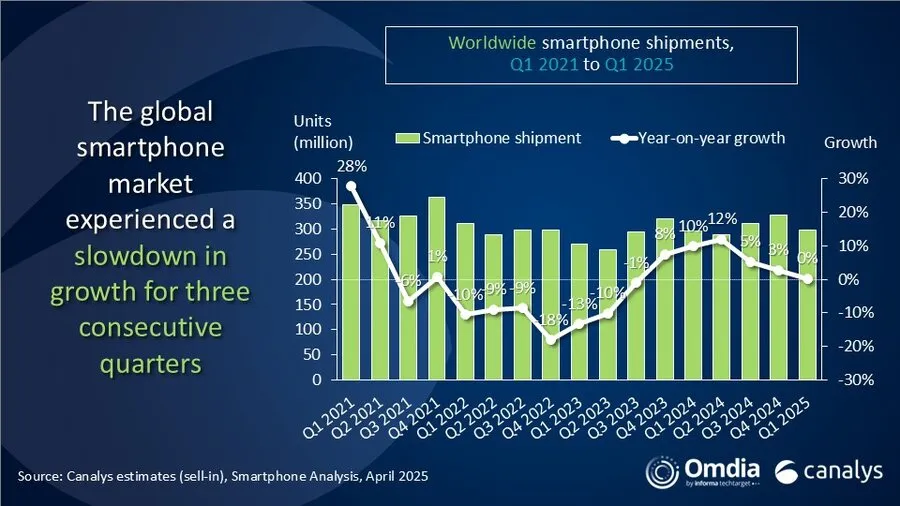

The global smartphone market saw only marginal growth of 0.2% in the first quarter of 2025, reaching 296.9 million shipments. This slowdown marks the third consecutive quarter of decelerating growth, as the peak replacement cycle subsided and vendors focused on managing inventory levels. Samsung held its leading position, supported by new flagship and affordable A-series launches, while Apple secured second place with strong performance in specific emerging markets. Xiaomi rounded out the top three, leveraging its ecosystem in Mainland China and overseas.

Contents

Read more about the global smartphone market

Key Takeaways:

- Global smartphone shipments grew by a mere 0.2% in Q1 2025.

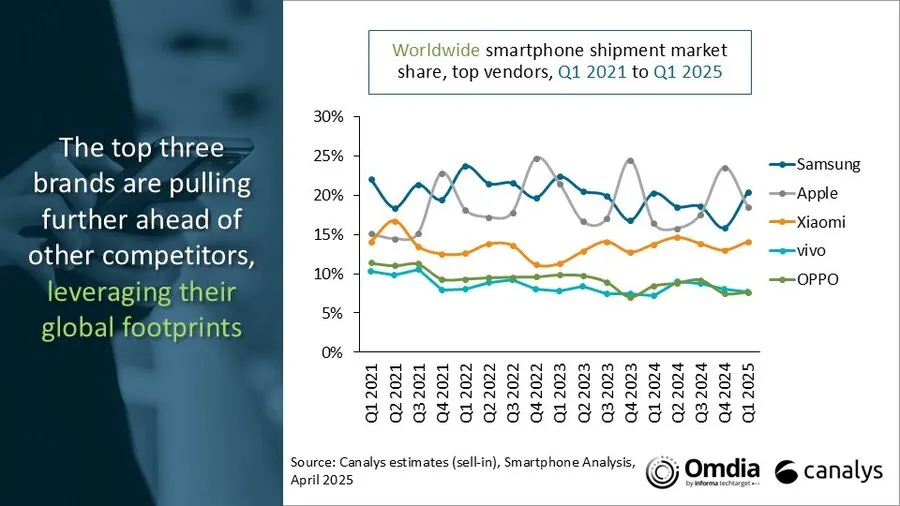

- Samsung, Apple, and Xiaomi remained the top three vendors.

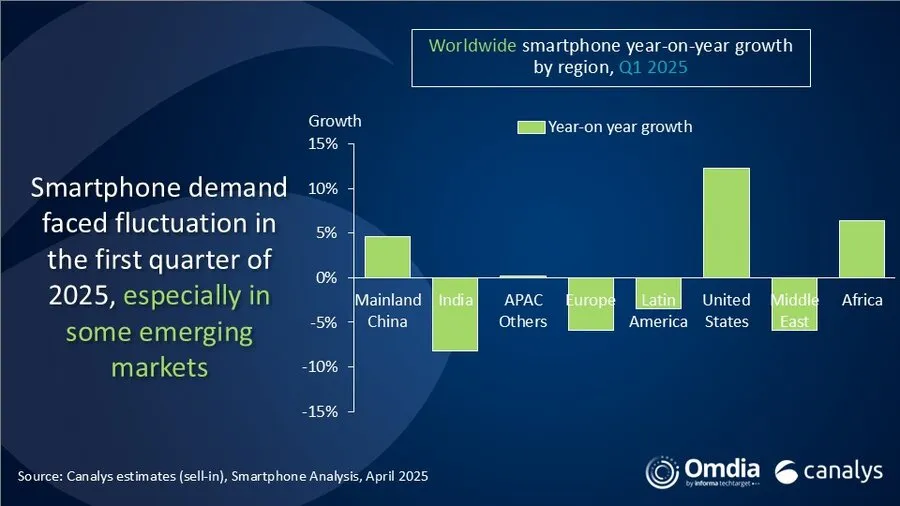

- Growth drivers shifted regionally, with declines in previously strong markets like India and Latin America, while the US, Mainland China, and Africa showed resilience.

- Inventory management and regional saturation impacted overall market dynamics.

- Brands maintain optimism for a recovery in the second half of 2025 despite ongoing challenges.

Market Performance Overview

The slight growth in Q1 2025 indicates a stabilization phase for the global smartphone market rather than a strong rebound. Following periods of pent-up demand driving replacements, particularly in value-focused segments, consumer purchasing cycles appear to be lengthening again. This, combined with vendors proactively managing stock levels to avoid oversupply issues seen in previous periods, contributed to the slower shipment volume.

Top Vendor Landscape

Samsung maintained its market leadership in Q1 2025, shipping 60.5 million units and holding a 20% market share. The company benefited from the launch of its latest high-end devices and the introduction of new, competitively priced models in its popular A-series, appealing to a broad customer base.

Apple secured the second position, shipping 55.0 million units and capturing 19% of the market share. Apple’s performance was notably strong in growth regions like emerging Asia Pacific markets and continued solid demand in the United States.

Xiaomi held third place with 41.8 million shipments, representing a 14% market share. The company leveraged its diverse portfolio and strong brand recognition, particularly in Mainland China and expanding its presence in emerging overseas markets through its ecosystem strategy.

vivo and OPPO followed, shipping 22.9 million and 22.7 million units respectively. The competitive landscape among the top players remains dynamic, with strategies focused on product mix, pricing, and channel partnerships proving crucial.

Bar chart showing global smartphone vendor shipments and market share for Q1 2025 compared to Q1 2024, highlighting Samsung, Apple, Xiaomi, vivo, and OPPO performance.

Bar chart showing global smartphone vendor shipments and market share for Q1 2025 compared to Q1 2024, highlighting Samsung, Apple, Xiaomi, vivo, and OPPO performance.

Shifting Regional Dynamics

The market displayed significant regional variation in Q1 2025. Markets that demonstrated robust growth in the past year, including India, Latin America, and the Middle East, experienced declines. Analysts attribute this to saturation as replacement demand for affordable and mid-range devices softened. Many Android vendors actively reduced inventory in these regions to clear channels for upcoming product launches and maintain stable pricing.

Europe also saw a dip after a brief recovery period. Vendors are grappling with elevated stock levels of flagship phones from the end of last year, alongside disruptions to lower-end product lines due to upcoming eco-design regulations impacting product specifications and costs.

Despite challenges, some regions presented positive trends. Mainland China’s market saw growth, partly fueled by government subsidy programs designed to stimulate consumer spending on electronics. Africa continued its upward trajectory, benefiting from vibrant retail activity and strategic market expansion efforts by vendors.

Within this complex environment, some brands found success through optimized product portfolios. vivo and HONOR, for instance, achieved double-digit growth in their overseas markets, with HONOR reaching a new high in its international shipments, demonstrating that targeted strategies can yield results even in a slow market.

A close-up image showing a hand interacting with a smartphone, representing diverse regional markets and product usage.

A close-up image showing a hand interacting with a smartphone, representing diverse regional markets and product usage.

The US Market Exception

The United States smartphone market stood out with strong 12% year-on-year growth in Q1 2025, primarily driven by Apple. This surge was partly influenced by Apple strategically increasing inventory in anticipation of potential future tariff policies.

While a significant portion of iPhones shipped to the US are still manufactured in Mainland China, production in India has rapidly scaled up towards the end of the quarter. This includes standard models of the iPhone 15 and 16 series, with acceleration also noted in the production of the premium 16 Pro series. Continued uncertainty surrounding reciprocal trade tariffs is expected to push Apple further towards shifting US-bound production to India to mitigate future risks.

Tariffs are also likely to impact the availability and pricing of entry-level smartphone devices in the US, potentially reducing the selection of lower-cost models and driving up the average selling price (ASP) across the market. These evolving trade dynamics create uncertainty not only for Apple but also for Android competitors. Pricing strategies, carrier bundle offers, and future product line structures will face significant pressure in this environment. The US market is forecast to experience considerable volatility over the next two to three quarters as inventory adjustments and fluctuating consumer confidence play out.

Abstract image featuring multiple smartphones and hands, illustrating market activity and consumer engagement in a specific region like the US.

Abstract image featuring multiple smartphones and hands, illustrating market activity and consumer engagement in a specific region like the US.

Outlook and Challenges Ahead

Despite the modest performance in Q1, major smartphone brands remain optimistic about a market rebound, particularly in Q2 and strengthening in the second half of 2025. Signs of gradual recovery were noted in markets like Southeast Asia and Latin America towards the end of the quarter. Decreasing inventory levels and planned mid-year launches of new mid-range and entry-level products contribute to this positive outlook.

However, significant challenges persist. Brands are being cautious with hardware upgrades in mass-market segments to manage rising production costs, requiring more precise strategies for product life cycles, pricing, and market entry. Competition in the mid-range segment ($200 to $400) is expected to intensify as vendors look for opportunities to increase their average selling prices. Furthermore, the potential for escalating global trade tensions could encourage more countries to prioritize localized smartphone manufacturing, adding potential investment and cost pressures for vendors operating globally.

In conclusion, Q1 2025 shows a smartphone market navigating complex regional shifts and inventory corrections after a period of strong replacement demand. While the overall growth was minimal, underlying trends in key markets like the US, China, and Africa offer pockets of opportunity. The path forward involves careful strategic adjustments to product portfolios, pricing, and supply chains, with the expectation of a more dynamic second half of the year despite ongoing economic and geopolitical uncertainties. Stay informed on how these trends develop.