Greater Toronto Area (GTA) new home sales plunged to an all-time low in April, according to data from Altus Group. This dramatic drop in demand, coupled with a significant rise in available homes, signals a deepening downturn in the market and puts further pressure on prices, although they have shown surprising resilience so far.

Contents

Key Takeaways:

- April 2025 saw the weakest new home sales month on record in the GTA.

- Inventory of new homes reached levels not seen in nearly a decade, resulting in 15 months of supply.

- Benchmark prices for single-family homes and condos have declined but remain elevated near 2021 levels.

- Weak demand is likely driven by persistent unaffordability and broader economic factors, rather than solely tariff concerns cited by some industry observers.

GTA New Home Sales Plummet to Historic Low

The demand for new homes in the GTA has reached an unprecedented nadir. Only 310 new homes were sold in April 2025, a staggering 72% decrease compared to the previous year and an 89% drop below the 10-year average. This figure marks the weakest monthly sales performance recorded in over 30 years of data.

Soaring Inventory Creates Strong Buyer’s Market

While sales have cratered, the supply of new homes continues to grow. Single-family home inventory increased by 33% year-over-year, adding to the existing large supply of condos. Total new home inventory reached 21,363 units in April, a 6.3% rise from the previous year.

This volume represents the highest level of inventory seen in nearly a decade. Given the current pace of sales, this equates to approximately 15 months of supply. A balanced market typically has only 4 to 6 months of inventory. The current levels firmly establish a strong buyer’s market, which historically exerts significant downward pressure on prices.

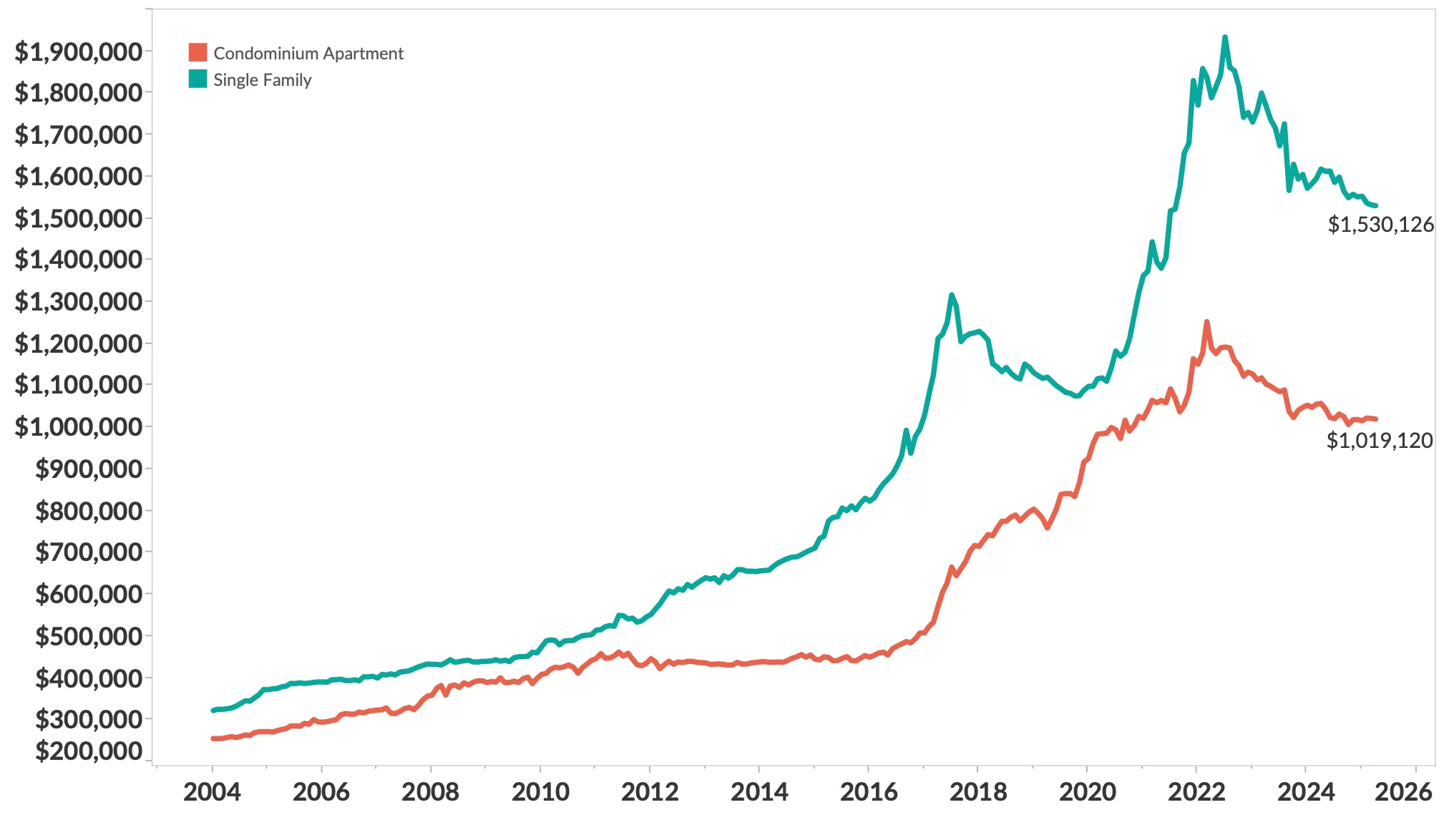

Prices Show Resilience Despite Market Weakness

Despite the record low demand and decade-high inventory, new home prices have not seen a proportional collapse, though they have declined moderately. The benchmark price for a typical new single-family home in the GTA fell by 5.4% from last year to $1.53 million in April. New condo prices also saw a decrease, dropping 3.6% year-over-year to $1.02 million.

Both segments are currently trading near their mid-2021 price levels, indicating a period of stagnation after significant gains during the pandemic housing boom. While off their peaks, prices remain considerably higher than pre-pandemic levels. This relative “stickiness” in pricing, despite overwhelming supply and weak demand, is a key factor contributing to the dramatic slowdown in sales.

GTA benchmark new home prices decline slightly in April 2025

GTA benchmark new home prices decline slightly in April 2025

What’s Behind the Demand Collapse?

Industry representatives have pointed to uncertainty surrounding tariff negotiations as a cause for buyer hesitation. Edward Jegg, research manager at Altus Group, noted that buyers “crave predictability, and the swirling uncertainty around tariffs is depriving would-be purchasers of the confidence they need.”

However, total year-to-date sales of just 1,569 homes are down 58% from last year, a period that predates the most recent increase in tariff discussion intensity. Furthermore, 2024 saw the weakest new home sales since the market crash of the 1990s, suggesting that the current issues are not solely tied to recent tariff talks.

A more likely explanation for the persistent weakness in GTA new home demand includes ongoing unaffordability challenges, rising unemployment, and demographic shifts such as prime-aged workers moving to provinces like Alberta. These broader economic and demographic factors likely have a more significant and lasting impact on the market than specific trade uncertainties.

Outlook: Continued Pressure on GTA New Home Market

With record low sales and near-record high inventory, the GTA new home market is firmly in buyer’s territory. The disconnect between soaring supply and relatively sticky prices explains the severe drop in demand. Looking ahead, the fundamental imbalance suggests that sustained price declines may be necessary to stimulate sales activity. Economic conditions, employment trends, and migration patterns will continue to be crucial factors shaping the market’s direction.