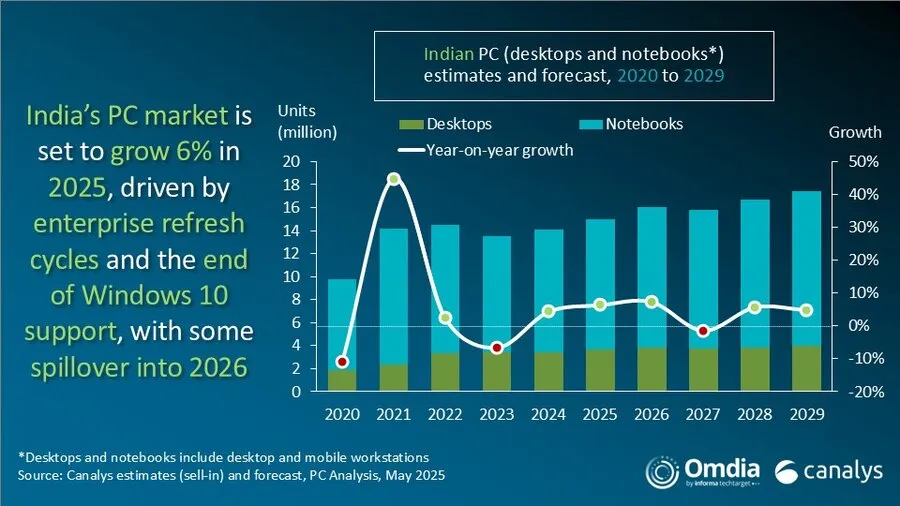

India’s personal computer market, excluding tablets, saw robust growth in the first quarter of 2025, with shipments rising 13% year-on-year to 3.3 million units. This surge was primarily fueled by a significant increase in notebook sales, highlighting the continuing importance of portable devices for both personal and professional use in the country. Despite the overall positive trend for PCs, the tablet market experienced a notable decline during the same period.

Contents

Key Takeaways:

- India PC shipments grew 13% in Q1 2025, reaching 3.3 million units.

- Notebooks led the growth, increasing 21% to 2.4 million units.

- Desktop shipments declined 3% to 906,000 units.

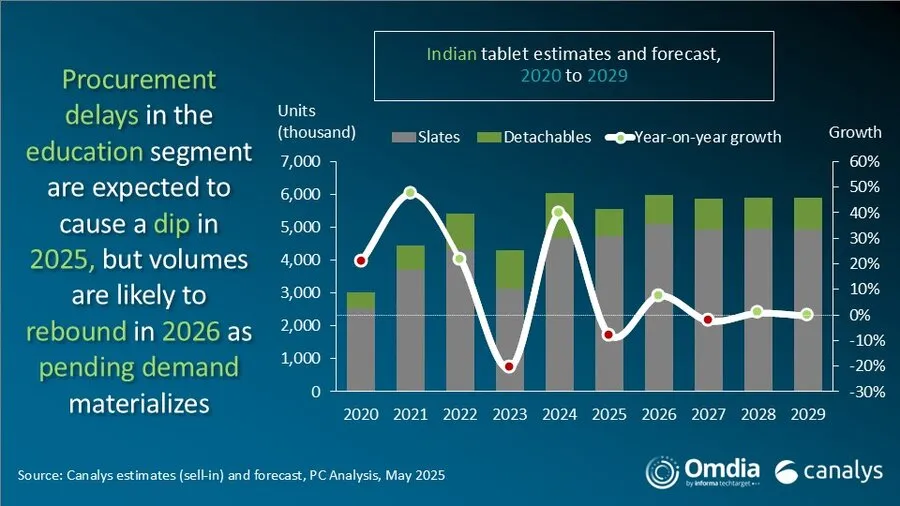

- Tablet shipments dropped 24% year-on-year to 1.0 million units.

- The overall PC market is forecast to grow 6% in 2025, while tablets are expected to contract 8%.

- AI-capable and premium notebooks showed strong growth, indicating demand for high-performance devices.

According to the latest research by Canalys, now part of Omdia, the dominant driver behind the PC market expansion was the notebook segment. Notebook shipments increased by a substantial 21%, reaching 2.4 million units, underscoring their role in enabling hybrid work models and meeting the rising productivity demands of consumers and businesses alike. In contrast, desktop shipments saw a 3% decline, totaling 906,000 units.

Graph showing India PC and tablet market performance and forecast data

Graph showing India PC and tablet market performance and forecast data

Diving Deeper into PC Segment Performance

Q1 2025 also marked a period of significant momentum for advanced computing devices. AI-capable notebooks, though starting from a smaller base, posted an impressive 253% year-on-year growth, signaling growing interest and adoption of AI features. Premium notebooks, defined as models costing over US$1,000, saw shipments jump by 49%. This indicates strong demand for high-performance machines capable of handling complex tasks, resonating with both consumers seeking multi-use value and enterprises viewing AI capabilities as essential.

The commercial PC segment grew by a solid 11%, largely powered by robust demand from private enterprises. Government demand, however, remained subdued during the quarter. The consumer segment outperformed the commercial market, with a 16% increase in shipments. This growth was attributed to effective Republic Day promotions and strong sales traction across various channels towards the end of March. Offline retail channels also experienced a resurgence, supported by vendor investments in dedicated brand stores and expanded presence in large-format retail outlets.

Mixed Fortunes for the Tablet Market

While PCs generally thrived, the Indian tablet market presented a more complex picture, facing a significant annual decline of 24% to 1.0 million units. This contraction was heavily influenced by performance differences across segments.

The consumer tablet segment showed resilience, growing 21% year-on-year. This growth was boosted by effective “back-to-school” marketing campaigns, particularly on online platforms, and vendors increasing their focus on offline retail presence. However, the commercial tablet market saw a sharp 54% decline. This downturn was primarily caused by delays in government and education tenders, which reduced institutional demand during the quarter. Despite this setback, the outlook for tablets remains optimistic, with the education segment expected to become the largest contributor to growth by the end of 2025.

Visual representation of India PC market segment performance or vendor market share in Q1 2025

Visual representation of India PC market segment performance or vendor market share in Q1 2025

Emerging Growth Hubs and Future Outlook

Beyond the major metropolitan areas, tier-two and tier-three cities are rapidly becoming critical engines for India’s PC industry growth. No longer considered just peripheral, these markets are now central to future expansion. As digital literacy deepens and access to education, broadband, and e-services expands, consumers in these cities are increasingly adopting PCs for productivity, learning, and entertainment. These buyers are typically value-conscious, making purchasing decisions after thorough research and prioritizing performance, durability, and after-sales service alongside the initial cost.

Looking ahead, 2025 is anticipated to be a pivotal year for both the PC and tablet markets in India, setting the stage for future shifts. While overall growth is projected to be moderate at around 2%, several key trends will shape the landscape:

- AI PC Mainstreaming: AI-capable PCs are expected to transition from a niche category to a mainstream offering as more enterprises incorporate them into their purchasing strategies.

- Steady Consumer Demand: Consumer demand is likely to remain stable, benefiting from coordinated online and offline sales channels and the continued rise of demand from tier-two and tier-three cities.

- “Make in India” Boost: Government initiatives, such as the Production Linked Incentive (PLI) scheme, are expected to yield tangible manufacturing gains, potentially leading more brands to announce expansion plans for local production.

- Premium and Gaming Segment Rise: As device refresh cycles accelerate, gaming and premium devices are set to play a more significant role in the market, although global economic uncertainties may temper commercial spending in specific sectors.

Overall, 2025 is viewed as a foundational year, building towards a more significant shift towards AI adoption, localization efforts, and a greater emphasis on value-driven demand across the Indian PC and tablet markets in 2026.