The US Dollar Index has fallen back to three-year lows, signaling a significant shift in currency markets. This move comes as major US stock indices, including the tech-heavy Nasdaq 100 and the S&P 500, extend their recent gains, with the Nasdaq hitting an all-time closing high. The market appears to be shrugging off earlier volatility, embracing a “risk-on” sentiment that often sees investors move away from safe-haven assets like the dollar.

Contents

This period of dollar weakness is influenced by divergent signals from the Federal Reserve regarding the future path of interest rates and broader market optimism. For investors, understanding this dynamic is crucial as it impacts everything from international trade costs to the performance of foreign investments.

Stock Markets Extend Rebound

US equities have maintained their upward momentum. The S&P 500 climbed 1.1% and is now less than 1% away from its own all-time high. The Nasdaq Composite saw a 1.4% rise, driven by continued strength in technology stocks. This rally suggests investor confidence remains high, favoring growth assets over defensive ones.

US Dollar Weakness Deepens

The broad-based decline in the US dollar is a key takeaway from recent market activity. The USD Index, which measures the dollar against a basket of major currencies, is trading at levels not seen in three years.

The most notable losses for the dollar were against traditional safe havens like the Japanese yen (JPY) and the Swiss franc (CHF), which typically strengthen during times of uncertainty but are gaining against the dollar even in this risk-on environment.

Federal Reserve’s Divided Stance on Rate Cuts

Adding complexity to the dollar’s outlook is the perceived division within the Federal Reserve regarding interest rate policy. While Chair Jerome Powell’s recent testimony to Congress did not explicitly signal immediate rate cuts, comments from other Fed officials, including Governor Waller and Vice Chair Bowman, highlight differing views. According to the Fed’s June projections, opinions are split almost evenly between those expecting two rate cuts in 2025 and those anticipating no change at all.

This split fuels debate over whether the Fed should remain strictly “data-dependent,” a stance adopted since 2022, or return to a more “forward-looking” approach. Critics argue a forward-looking bias previously delayed rate hikes. This uncertainty about the future path of US interest rates weighs heavily on the dollar.

Dollar Declines Against Asian Currencies

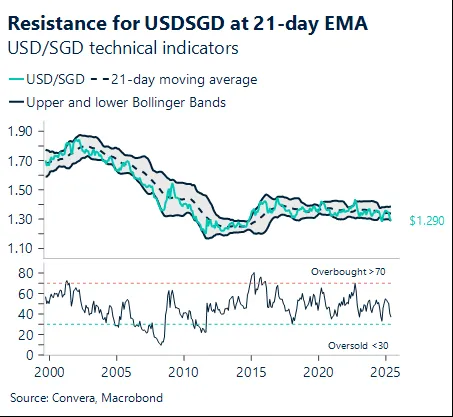

The US dollar also lost ground against several Asian currencies. The Singapore dollar (SGD) strengthened against the greenback, causing the USD/SGD pair to fall. The pair is now trading just 0.5% above its decade low recorded in June. The Chinese yuan (CNH) also saw gains against the dollar, with the USD/CNH hitting 10-month lows. These movements reflect regional economic dynamics and capital flows alongside the broader dollar weakness.

Technical chart showing the USD/SGD exchange rate testing a key resistance level at the 121-day Exponential Moving Average

Technical chart showing the USD/SGD exchange rate testing a key resistance level at the 121-day Exponential Moving Average

Other Currency Movements: Kiwi Rebounds

Beyond the major pairs, the New Zealand dollar (NZD) saw a significant rebound. This occurred amidst news related to a potential ceasefire agreement in the Middle East.

Although reports conflicted and hostilities continued, markets reacted initially to the headline. The NZD bounced off a key technical level (the 200-day EMA) and is approaching another significant level (the 21-day EMA), suggesting potential upward momentum. Oil prices, sensitive to geopolitical events, also extended their decline following the initial announcement.

Table summarizing seven-day rolling currency performance trends and trading ranges for major global currencies

Table summarizing seven-day rolling currency performance trends and trading ranges for major global currencies

Looking Ahead: Key Risk Events

Investors will be monitoring upcoming economic data and central bank commentary for further clues on market direction. The calendar for the rest of the week includes potential market-moving events that could influence currency and stock market trends.

Conclusion: What’s Next for the Dollar?

The US dollar’s retreat to multi-year lows reflects a confluence of factors: a robust stock market rally indicating strong risk appetite, and ongoing uncertainty surrounding the Federal Reserve’s interest rate trajectory. While US stocks are nearing peak levels, the dollar’s underperformance suggests that international investors and currency traders are either pricing in potential rate cuts or shifting capital elsewhere.

The divided views at the Fed remain a critical variable. Markets will be closely watching future data releases and official statements for clearer signals. For now, the trend points towards continued pressure on the dollar relative to many other currencies. Keep an eye on upcoming economic indicators and central bank speeches for potential shifts in this dynamic.